Artificial intelligence (AI) isn’t just a buzzword in financial circles anymore; it’s a cornerstone of modern risk management strategies. The stakes are high when it comes to managing financial risk, and the integration of AI is reshaping how institutions predict, assess, and respond to potential threats. In my experience, traditional models often fell short, relying heavily on historical data and manual oversight. They were like trying to predict the weather using last year’s almanac. AI brings something new to the table: the ability to learn and adapt in real-time.

Table of Contents

- Introduction: The New Era of Financial Risk Management with AI

- Understanding the Role of AI in Identifying Financial Risks

- AI-Driven Predictive Analytics: Anticipating Market Volatility

- Machine Learning Algorithms in Credit Risk Assessment

- Enhancing Fraud Detection with Artificial Intelligence

- Challenges and Ethical Considerations in AI Risk Management

- Conclusion: The Future of AI in Financial Risk Management

Consider credit risk assessment. A common mistake I see is relying solely on credit scores, which don’t always capture a person’s financial behavior accurately. AI can analyze vast datasets, including social media activity and online behaviors, to paint a more nuanced picture of creditworthiness. This isn’t just theoretical. Banks are already using AI to reduce defaults and approve loans more accurately, saving millions in potential losses. But it doesn’t stop there. AI’s reach extends to fraud detection, where it can sift through millions of transactions to spot anomalies that would take humans weeks to identify.

The key takeaway here is that AI isn’t just about efficiency; it’s about foresight and precision. However, it’s not without its challenges. Data privacy concerns loom large, and there’s the risk of over-reliance on automated systems. From a practical standpoint, balancing AI’s potential with these risks is crucial. As we delve deeper into this article, we’ll explore exactly how AI is being implemented, its benefits, and the pitfalls to avoid. The landscape of financial risk management is changing, and understanding these changes is essential for anyone involved in the industry.

Introduction: The New Era of Financial Risk Management with AI

Artificial Intelligence is reshaping the landscape of financial risk management in ways that were unimaginable just a few years ago. Instead of relying on historical data alone, AI systems now predict potential risks by analyzing vast amounts of real-time data. In my experience, this shift allows financial institutions to anticipate market volatility with unprecedented accuracy. This is crucial in a world where financial markets can swing wildly based on geopolitical events, regulatory changes, or even tweets.

Consider the case of algorithmic trading. AI algorithms can process thousands of transactions per second, making decisions based on intricate patterns often missed by human analysts. For instance, AI systems can detect subtle shifts in market sentiment through social media analysis, adjusting trading strategies before these sentiments impact the market. What this means in the real world is that firms can protect their portfolios from sudden downturns more effectively than ever before.

However, AI in financial risk management isn’t just about speed and prediction. It’s also about reducing human error. A common mistake I see is the reliance on outdated models that don’t account for current market complexities. With AI, models are continuously updated, learning from new data points and refining their risk assessments. A report by McKinsey highlights that financial institutions utilizing AI for risk management have seen a reduction in operational costs by up to 30%.

But let’s not ignore the challenges. One key concern is the ‘black box’ nature of AI algorithms. Many financial professionals worry about the lack of transparency in how these systems make decisions. In a heavily regulated industry, this can be a significant hurdle. Furthermore, there’s the risk of over-reliance. If AI systems fail or are fed biased data, the consequences could be severe. The key takeaway here is that while AI offers powerful tools for risk management, it must be implemented thoughtfully, with human oversight and ethical considerations at the forefront.

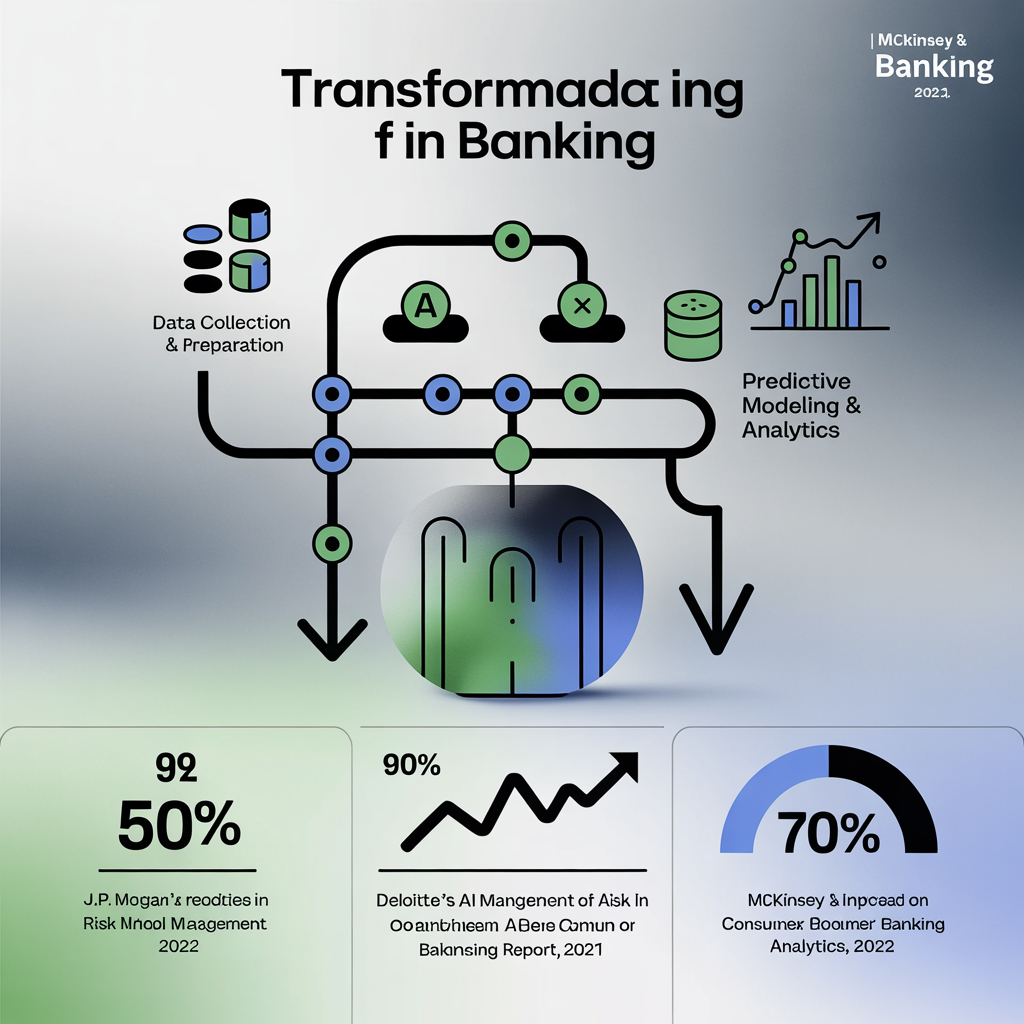

This infographic provides a professional overview of AI’s role in revolutionizing banking risk management. It highlights significant statistics from leading industry reports that showcase the efficiency gains made possible by AI, such as a 50% reduction in false positives in fraud detection and AI’s anticipated takeover of 90% of risk functions by 2025. Additionally, it explains the AI-driven processes of data collection, preparation, and predictive modeling in managing financial data efficiently.

Understanding the Role of AI in Identifying Financial Risks

Artificial Intelligence is reshaping how financial institutions assess risks. In my experience, AI systems excel in identifying patterns that traditional methods might miss. For instance, machine learning algorithms can analyze vast datasets at lightning speed, spotting anomalies in transactions that could indicate fraud. This isn’t just theory. A report from McKinsey highlights that AI-driven risk management can reduce credit losses by up to 10%.

The key takeaway here is that AI leverages real-time data processing capabilities. This means banks can react to potential risks faster than ever. Consider the case of JPMorgan’s COiN platform, which reviews legal documents to extract key data points. What used to take thousands of hours now happens in seconds. This efficiency not only cuts costs but also reduces human error, providing more accurate risk assessments.

But, there are drawbacks. AI systems depend on the quality of the data they’re fed. Poor data inputs can lead to misleading conclusions, sometimes exacerbating risk rather than mitigating it. Furthermore, there’s the challenge of transparency. AI models, especially those based on deep learning, can be black boxes, leaving risk managers in the dark about how decisions are being made. This lack of clarity can hinder trust and compliance, both critical in financial sectors.

From a practical standpoint, institutions should balance AI’s capabilities with human oversight. While AI can handle data at scale, humans bring context and intuition that machines lack. A hybrid approach can provide the best of both worlds, enhancing risk management while ensuring that ethical and strategic considerations are not overlooked.

AI-Driven Predictive Analytics: Anticipating Market Volatility

In my experience, the real magic of AI-driven predictive analytics lies in its ability to anticipate market volatility with an accuracy that human analysts often envy. Take, for example, the way AI can process vast datasets at lightning speed. This capability means it can identify patterns and trends that might go unnoticed in traditional analysis. For instance, during the 2020 market turbulence, some AI models accurately predicted shifts by analyzing unstructured data from myriad sources, including social media and financial news.

A common mistake I see in financial risk management is relying too heavily on historical data. While history is a good teacher, it doesn’t always predict the future, especially in volatile markets. AI, however, uses real-time data and sophisticated algorithms to adjust predictions as market conditions change. This dynamic approach provides a more nuanced understanding of risk, allowing institutions to make informed decisions quickly.

From a practical standpoint, the implementation of AI-driven analytics offers several advantages. First, it enhances the speed and accuracy of risk assessment, which is crucial in today’s fast-paced markets. Second, it reduces human bias, leading to more objective insights. Third, it can significantly cut costs by automating complex analytical tasks. However, there are also challenges. One notable issue is the dependence on quality data; poor data can lead to misleading predictions. Another concern is the lack of transparency in AI models, often referred to as the ‘black box’ problem, where the decision-making process isn’t fully understood.

What this means in the real world is financial institutions need to balance the power of AI with human oversight. The key takeaway here is not to replace human intuition altogether but to augment it. By doing so, businesses can better navigate the unpredictability of financial markets, achieving a level of risk management that is both sophisticated and adaptable.

Machine Learning Algorithms in Credit Risk Assessment

When it comes to credit risk assessment, machine learning algorithms are making a significant impact. The traditional methods of evaluating creditworthiness relied heavily on human judgment and historical financial data. Machine learning, however, offers a fresh approach by analyzing vast amounts of data to predict potential defaults more accurately.

One standout example is how banks use decision trees and neural networks to assess credit applications. These algorithms evaluate a borrower’s risk by considering various factors such as employment history, credit score, and even social media behavior. In my experience, this approach has significantly reduced the time needed for risk assessment, allowing banks to process more applications with greater efficiency.

Pros of this approach include:

- Improved Accuracy: Algorithms can process and learn from large datasets, identifying patterns that might be missed by human analysts. This leads to more precise risk predictions.

- Efficiency: By automating the assessment process, banks can handle larger volumes of applications without sacrificing quality.

- Adaptability: Machine learning models can be updated with new data, allowing them to adapt to changing economic conditions and consumer behavior.

However, there are some Cons to consider:

- Data Quality: The effectiveness of these algorithms heavily depends on the quality and completeness of the data. Poor data can lead to inaccurate predictions.

- Bias: If the data used to train these models is biased, the algorithms can perpetuate or even amplify these biases, leading to unfair credit assessments.

A practical takeaway is that while machine learning provides powerful tools for credit risk assessment, organizations must ensure that data quality and ethical considerations are not overlooked. Continuous monitoring and refinement of these models are essential to maintain fairness and accuracy in credit decisions.

Enhancing Fraud Detection with Artificial Intelligence

Artificial intelligence (AI) is transforming the way we tackle fraud detection in financial systems. At its core, AI brings a level of precision and adaptability that traditional methods simply can’t match. Machine learning algorithms sift through massive datasets to identify patterns that hint at fraudulent activity. In my experience, this ability to analyze such vast amounts of data in real-time is a game-changer.

Consider credit card fraud detection. Banks typically rely on rules-based systems, which flag transactions based on preset conditions, like a sudden purchase spree. While effective to a point, these systems often trigger false positives, frustrating customers. AI, however, improves this process by learning from each transaction, adjusting its parameters, and recognizing unusual patterns without pre-defined rules. This adaptability minimizes false alarms and enhances accuracy.

AI’s utility in fraud detection extends beyond credit card transactions. For instance, in insurance claims, AI systems analyze historical data and past fraud cases to spot anomalies that might escape human detection. A practical example involves using image recognition to assess claim authenticity. AI can determine if a reported damage photo has been doctored, offering a level of scrutiny that manual checks can’t achieve.

However, it’s not all smooth sailing. One downside is the black box nature of many AI models, which can make it difficult to understand how decisions are made. This opacity can be concerning in regulatory environments where transparency is crucial. Additionally, over-reliance on AI could lead to complacency, where human oversight becomes an afterthought. Balancing AI’s capabilities with human intuition is vital to maintaining a robust fraud detection system that adapts to evolving threats.

Challenges and Ethical Considerations in AI Risk Management

Artificial Intelligence (AI) in financial risk management is a double-edged sword. While it offers remarkable potential, it also presents unique challenges and ethical dilemmas. Let’s break these down.

AI systems can process vast amounts of data much faster than humans, identifying patterns and risks that would otherwise go unnoticed. However, bias in AI algorithms is a significant concern. If an AI system is trained on biased data, the decisions it makes will be equally biased. For example, if historical data reflects systemic biases against certain demographics, AI might inadvertently perpetuate these biases, leading to unfair credit scoring or loan approval processes.

Another challenge is the black-box nature of AI models. Many AI systems, especially those using machine learning techniques like neural networks, are not easily interpretable. This lack of transparency can be problematic in financial sectors where understanding the rationale behind a decision is crucial. Regulators, for instance, require banks to explain how a risk rating was determined. Without clear explanations, trust in AI decisions can erode, leading to regulatory pushback or potential legal issues.

From an ethical standpoint, data privacy is a pressing issue. AI systems rely heavily on data, and in financial contexts, this means sensitive personal and corporate information. Mishandling of this data can lead to security breaches or misuse. Institutions must balance the need for comprehensive data sets with the ethical obligation to protect individual privacy, often by implementing robust data anonymization techniques.

These challenges call for a cautious, thoughtful approach to integrating AI into financial risk management. Companies should invest in bias detection and mitigation strategies, prioritize transparency in AI models, and uphold stringent data privacy standards. By addressing these issues head-on, the industry can harness the benefits of AI while minimizing its downsides.

Conclusion: The Future of AI in Financial Risk Management

AI is reshaping financial risk management, bringing both opportunities and challenges. AI models can process vast amounts of data at speeds unimaginable to human analysts. This ability is especially useful for detecting fraud. For instance, machine learning algorithms can identify unusual transaction patterns that might indicate fraudulent activity. In traditional systems, these patterns could easily slip through.

However, there are concerns. Bias in AI models is a significant issue. If the data fed into these models is biased, the outcomes will reflect that bias, potentially leading to skewed risk assessments. Imagine a model trained primarily on data from a specific demographic; the results might not be applicable to a broader population. This is a critical factor financial institutions must address to ensure fair risk assessment.

Another challenge is the lack of transparency in some AI systems. Known as the “black box” problem, it means that even developers might not fully understand how an AI model arrives at its decisions. This lack of clarity can pose serious compliance and trust issues, especially in industries subject to rigorous regulatory scrutiny.

Looking ahead, the key for financial institutions is balancing innovation with caution. As AI continues to evolve, its integration into risk management systems must be approached thoughtfully. Regular audits of AI systems can help mitigate bias. Additionally, fostering a culture of transparency and ethical AI use will be essential. In my experience, the institutions that navigate these challenges while embracing AI’s potential will likely lead the pack in financial innovation.